The Importance of Creating Income

Let me start by asking you a question…

How are you going to get to where you want to go in life?

Now I don’t know what your answer is, nor do I know your situation. You might be a 35 year old with a great career and a clear path to your golden years. You might also be 63 years old and recently furloughed, replaced by a 22 year old that knows a fraction of what you do. It really doesn’t matter where you currently are in life, nor does your current situation have any bearing on it, because all situations share the same need:

To get where you want to go in life, you need to generate income.

Notice that I didn’t say “a lot of money” nor did I challenge you to come up with a massive figure that you’re supposed to carry around. Sure, having a big pile of money solves a lot of problems for you if you already have it. But for most of us, that reality changed over the past few years. We’re not focused on generating income, we’ve been told to think that we need to grow ourselves a huge pile of money. And we’ve been taught – ironically, not by our education system, but by watching TV commercials – that the magic formula to attaining this “pile of money” is to create ourselves a “great portfolio.” If you believe the TV ads put out by the brokerage houses, you can be an infant in a crib or a guy sitting outside with a laptop and build this wondrous collection of stocks and bonds which magically goes up every month.

Sure, it’s certainly possible. But what do you do when the market no longer supports your “great portfolio?” Markets don’t always move straight up, and no “green line” will protect you against that if your portfolio is not risk-adjusted.

You see, most individual stock traders don’t know how to build income, nor do they see a need for it. The dream that they’ve been sold is that they can ride the market up and build their portfolio to “their number” so they can magically take their funds out of risk at exactly the right time to fund their retirement for as long as they need it.

Wait, haven’t we just seen two recessions in the past two decades? Haven’t we seen enough unexpected downdrafts and corrections that have wiped out trillions in investor wealth from investors trying to “ride out” the pullback and not knowing when to get out? If your primary strategy is to time the market by buying low and selling high, and selling out at the very top, be aware that this is a very, very difficult game that you’re playing and that you’re probably not managing your risk nearly as well as you need to. You’re betting the farm that you’ll have enough of a lump sum someday to turn into an income source.

What if we were able to generate cash flow and income right now?

Think about what that would mean to our ability to grow our account incrementally, through the power of compounding. None other than Albert Einstein was quoted to have said: “The most powerful force in the universe is compound interest.” Warren Buffett will not consider investing in a company unless it can prove the ability to compound their earnings growth through reinvestment.

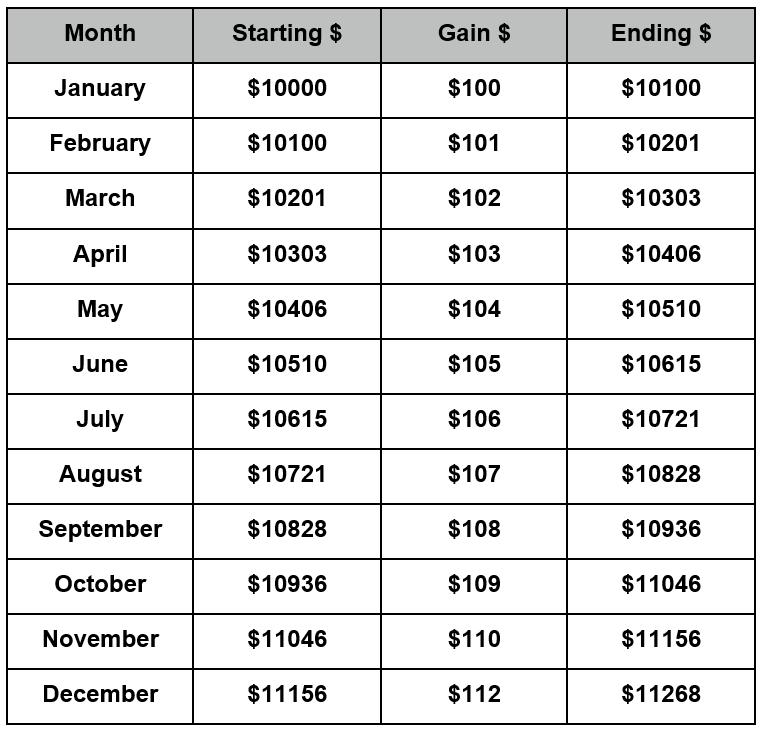

Quick, if I earned 1% on my capital every month, what would my annual return be? Most will quickly say “12%” without thinking through the question, but let’s take a look at the power of compounding income growth if we were able to just earn 1% a month on our starting capital of $10,000:

Figure 1

In this example we showed how a very conservative 1% monthly return ends up turning into an annualized 12.67% return, larger than a simple linear addition of the monthly returns due to the re-investment or compounding. Higher monthly gains can produce even more compound growth; for example, a 3% monthly return on capital produces not just 36%, but a compounded annual return of about 42.5%! We would double our capital every two years with that kind of return.

Can we do that kind of performance with stocks? Well, it’s certainly possible, but unrealistic to earn consistent returns. Dividends just aren’t paid often enough to enjoy the true power of compounding. And with typical annual dividend yields of 3% or so (ex: PG), it just won’t provide the income acceleration that we’re looking for, nor do dividend-paying stocks usually show much growth in the share price.

So it’s clear what we need to do to develop income:

- Find an investment vehicle that we understand, without having to understand the company’s business model or financial statements.

- Find an investment vehicle that allows us to earn monthly income.

- Find an investment vehicle where we clearly understand the risks, and can manage them proactively.

- Find an investment vehicle where we can re-invest our income to enjoy the compounding effect.

As you probably expected me to say, the investment vehicle that allows us to accomplish those objectives are OPTIONS. How can we create an income stream through options?

Methods of Creating Income

When you think of generating Income, what are the typical methods and strategies that you hear floating around out there? Here is a list of the usual suspects:

Salary – of course we think of trading our time and skills in exchange for a salary, which generates income. However it’s extremely high-effort and may not be realistic in our retirement years.

Stocks – certain stocks generate a quarterly dividend which can generate a regular check.

Preferred Stock Shares – some companies offer preferred shares in addition to common stock shares; these typically offer a larger dividend payment in exchange for a higher share price.

Real Estate Rental – owning all or part of a property and receiving rental income.

REITs or Real Estate Investment Trusts – these are based on a portfolio of real estate, where income is passed along to shareholders.

Bonds – generally pay interest twice a year.

Annuities – depends on the structure, but the back-end is a set income stream for a period of time after you pay in for an agreed-upon timeframe.

Limited Partnerships – income is passed along to the partners.

The whole idea behind investing is that we someday replace our existing salary income with some other type of generated income, so that we can travel the world and enjoy retirement. And for those really on the ball, we could even generate a stream of income to replace our existing salary and break the paradigm of having to wait until we’re 65 before we can retire.

I think that the “typical” retirement income strategies might have worked out OK until a few years ago, but some things have changed recently that have put a damper on these methods:

- Interest rates are so low these days that bond income is insufficient;

- The real estate market is struggling to recover;

- Stocks have been more volatile/unpredictable over the past 16 years than any time since the Great Depression.

As a result, we have a huge number of retirees—or people closing in on retirement age—that have not built up enough capital to generate living income.

And we all know that Social Security payments don’t cut it. We have parents moving back in with their children for the first time in generations. It’s reality.

Why are these situations happening? In simple terms, it’s because the “old” systems discussed above are not working in today’s paradigm. And many of you have already figured this out and have tried to take control by learning to trade your own portfolio. We all arrive at this step due to the many powerful media messages that we’re bombarded by constantly:

- “YOU CANNOT TIME THE MARKET. BUY GOOD QUALITY STOCKS FOR THE LONG HAUL.

- GET THE TOOLS AND RESEARCH THAT YOU NEED TO MAKE INFORMED DECISIONS.

- ALLOW US TO HELP YOU REACH YOUR INVESTMENT GOALS.”

If it was really that simple to just follow a “green path” to reach your retirement goals, then you wouldn’t be here, either. After watching one of the well-respected companies in the “managed money” space crush my retirement portfolio to 30% of its former worth, I knew that no one had as much of a vested interest in my future as I did. I found out that they didn’t have a clue how to grow an account unless the market was going straight up!

So if you’re going to wrestle this assignment back into your control, how are you going to generate consistent income? Are you really going to sign up as a limited partner with firms that you don’t know what they do? Are you going to expose yourself to the risk of a REIT? Are you going to depend on the quarterly dividend payment of a stock that has flatlined and not going up in value?

If you follow all of the traditional income strategies above, you end up investing in things you don’t understand and becoming a Jack of All Trades and a Master of None. And do you really want to respond to your tenant’s complaints of blocked pipes at 3 a.m? There’s got to be a better way. All of us are running out of time; let’s see how we can get some of it back.

Generating an Income Stream from the Market

Before we can start to pull out a consistent income stream from the market, it’s important that we understand what we’re doing wrong first. Yes, “we” who have gotten most of our education about the stock market through watching E*Trade commercials and TV personalities like Jim Cramer.

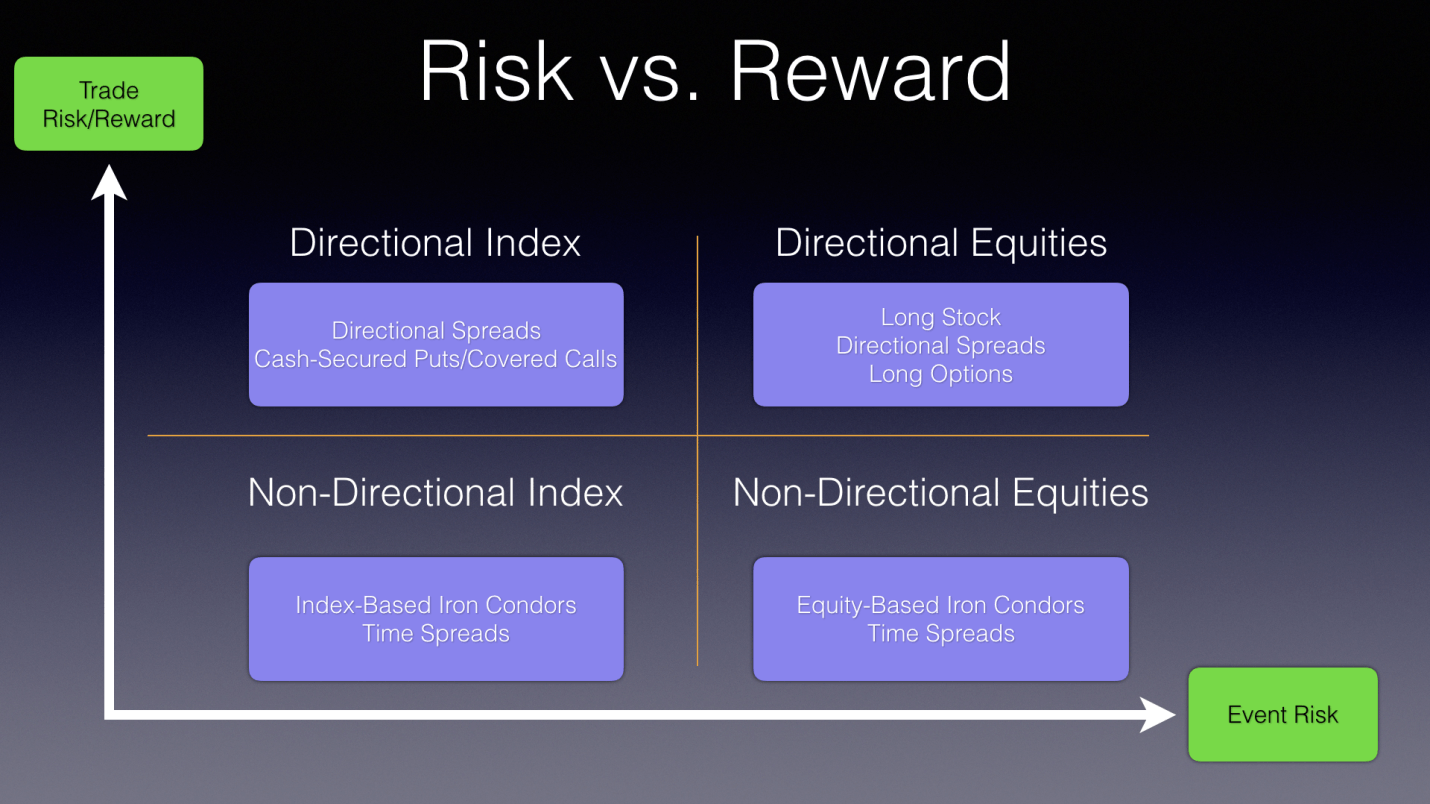

Let’s step back from the process for a second and classify our trades in a couple of different dimensions:

Trade Risk/Reward: When we’re trading, there is no reward without risk. Conversely, if there is no risk, there is no reward. Generally, the more risks that you face on a trade, the higher the reward should be. Usually, the risk/reward equation is a function of how “directional” the trade set-up is, with a reward being placed on being “right” directionally.

Event Risk: This is the risk that some event could come along unexpectedly and influence the supply or demand for your trade. This could have a positive or negative impact on the price, you just don’t know ahead of time.

These are not the only two dimensions that we can plot our trades on, but these are very important. Let’s combine these dimensions by plotting the risk/reward of a trade on the vertical axis of a chart in Figure 2, and let’s use event risk as the variable on the horizontal axis.

Figure 2

So risk/reward increases as we go higher on the vertical axis, and event risk increases as we move to the right on the horizontal axis.

Now let’s fill in the quadrants, starting with risk/reward:

Non-directional trades are going to have less risk and less reward than directional trades are, so the bottom two quadrants are non-directional and the top two quadrants are directional.

Now let’s rank positions by event risk:

Index trades are going to have less event risk than individual equities due to the lack of earnings reports, management changes, warnings, surprises, etc.

When we put it all together, we can see that the quadrant with the least amount of risk/reward as well as the quadrant with the least amount of event risk is the lower-left quadrant. Conversely, the quadrant with the highest risk/reward and event risk is the upper right quadrant.

Now let’s start to fill in the quadrants with actual trading strategies:

Lower Left: non-directional index-based trades like Iron Condors and Time Spreads.

Lower Right: non-directional equity-based trades like Iron Condors and Time Spreads.

Upper Left: directional index-based trades like ETF/futures swing trades, weekly spreads, debit spreads, and Covered Calls/Naked Puts.

Upper Right: directional equity-based trades like stock, single-stock futures, long options, etc.

Question for you: In what quadrant do 99% of all newer traders begin their trading careers?

You guessed it, the upper-right quadrant, the riskiest quadrant of the four.

Next Question: Which quadrant should traders begin their careers in?

Where else can you find a profession where all of the entry-level trainees start right at the top level? It’s like saying that you think you can swing a bat, so you’d like to try out for your local Major League baseball team. You hit a golf ball at the range pretty well the other day (one out of a whole bucket) so you feel it’s time to tee it up at the Master’s in Augusta, and you check your mail every day for your invitation. Your son just passed his driver’s permit, so it’s time to put him in the Ferrari. Example after example where we all have tons of common sense—except when it comes to trading the Market!

And believe me, when you place your position in the market, you’re going up against the very best in the world, every day. There are no minor leagues in trading.

Now, maybe you didn’t recognize the names of some of those trading strategies; that’s OK, we’ll get to those shortly.

Creating the Income Pyramid

So far you’ve learned that you should be trading non-directional index trades to start, whatever those are. Does that mean that we should NOT be trading stocks or other valid strategies? NO, of course not…all in good time, and when you’ve “earned the right.” It’s time to build our trading “house,” which happens to be in the shape of a pyramid.

When you build a house, what is the most important floor of the building? The first floor with the family room and kitchen? The second floor with the bedrooms?

How about the FOUNDATION?

Without a doubt that’s the most important floor of the house; without a solid foundation, every floor above it will sag/settle and show cracks. It’s a nightmare that never ends. The same thing applies to your trading. You must build a solid foundation for your trading business that is solid as a rock, and is available month after month. Once you set the foundation, you can build on top of it. And this is exactly where our “Income Pyramid” comes in.

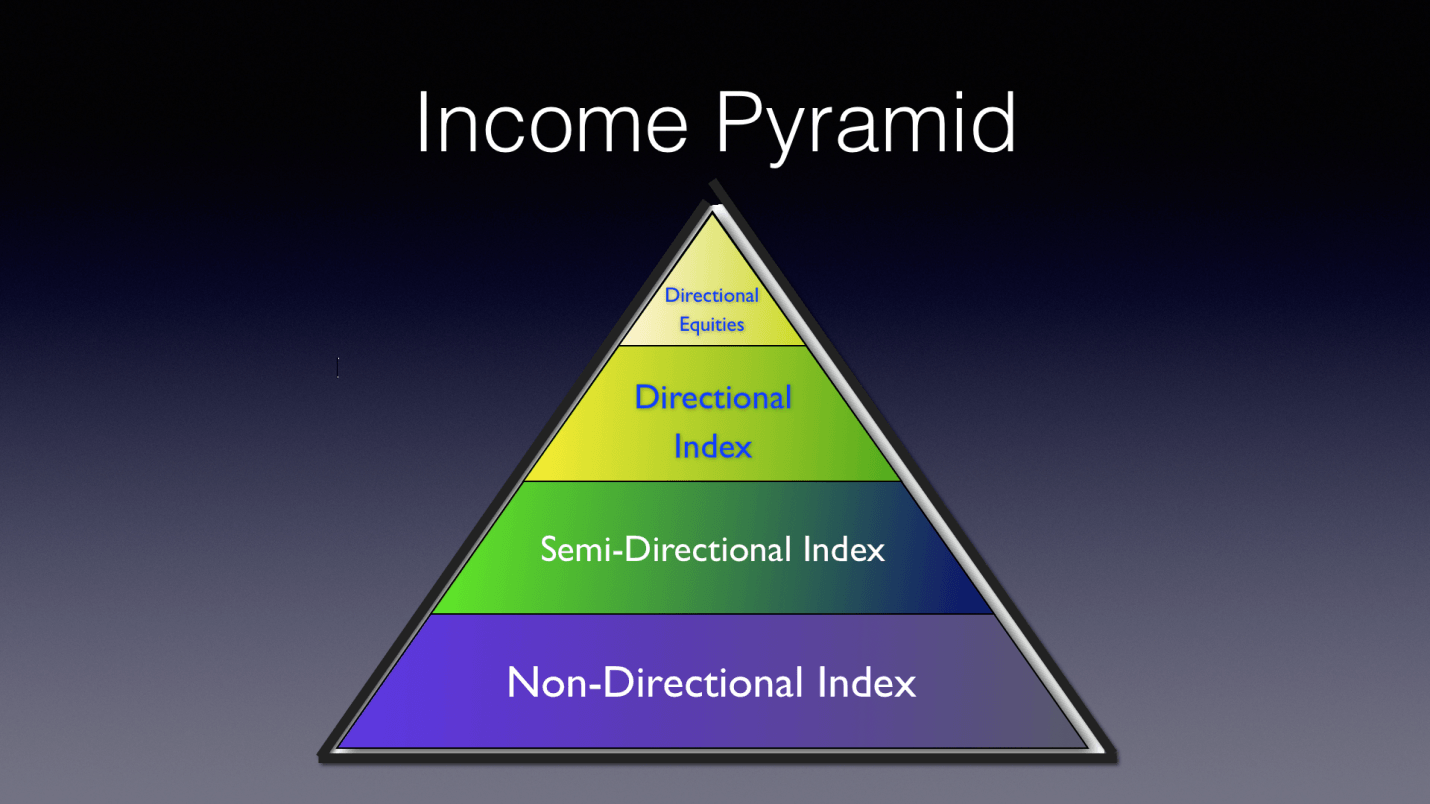

Figure 3

We will set up the “floors” of this Income Pyramid in this manner, using the appropriate trading strategy at each level. The shape of the pyramid represents the amount of capital that we will bring to bear with each strategy as well.

Each of the floors will have the following income-earning strategies in play:

Foundation: non-directional index strategies like High Probability and Low Probability Iron Condors or Time Spreads like Calendars and Diagonal Spreads, being played on an index chart, can offer consistent monthly income and are limited risk/limited reward yet yield excellent probabilities.

First Level: semi-directional index strategies like cash-secured Puts/Covered Calls can be played during favorable trends using index charts, also offering consistent monthly income with slightly higher risks and higher potential rewards vs the non-directional trades. These trades do require somewhat of a positive trend to be effective.

Second Level: directional index strategies like long stock, index futures, and/or directional and weekly spread strategies offer occasional, higher-reward opportunities when high probability set-ups are present.

Third Level: directional equity stock strategies using stocks or directional spreads offer occasional, high-reward “home run” opportunities when high probability set-ups are present.

When you put all of these strategies together, you have a vertically-integrated set of trading strategies that all work together harmoniously to provide consistent streams of income without much regard to what the underlying market is doing; this is why I call it the “Income Pyramid.”

Something else that the pyramid represents is your progression as a trader; once you master each level, you will “earn the right” to move to the next level and attain higher potential returns. With this in mind, notice how trading individual stocks is at the very top of the pyramid, using the smallest amount of capital.

Isn’t this exactly the opposite of what you have been doing to this point?

It was for me when I first started trading, and it’s the same for 99% of traders that I come across. It requires you to break your current paradigm of thinking that the way that you must trade is to find that “needle in the haystack” stock that Goldman Sachs and their billions in research somehow overlooked. One of the COOLEST things about this income pyramid is that the first three levels can be played using ONE STOCK CHART, like the S&P 500 or the Russell 2000. I cannot possibly be an expert in 6,000 individual stocks but I can get to know one or two charts really, really well.

And you can, too.

ABOUT THE AUTHOR

Doc Severson has been actively trading the U.S. stock, futures, and options markets since the mid-90s and his specialty is trading the U.S. equity options market. With a background in engineering, Doc is able to break down complex market ideas into an easily digestible format.

For the past ten years he has provided daily insights and market analysis via market newsletters, as well as helping students learn the complexities and edges of the options markets through live training and courses. Doc can be found at TheoTrade.com, daily in TheoChat® and twice per week in TheoNight® providing market insights and trade ideas.

SPECIAL OFFER FROM THEOTRADE

FREE ebook: The Rebel’s Guide to Options Trading

FREE ebook: The Rebel’s Guide to Options Trading

Here’s what’s inside this brand new ebook:

- How to use options to be the house because as we know the house always wins

- How to protect your portfolio from any shock to the markets

- How to generate consistent returns in the market while minimizing your risk

- How to put probabilities on your side to win 85% of the time using options

- How to use high probability options strategies so you don’t have to rely on coin flip returns