By Jody Chudley, Financial Analyst

Some opportunities are just too obvious to pass up.

On January 10th we e-mailed you and pounded the table on the commodity sector.

Why?

Because we believed that there was conclusive evidence that the entire sector was unbelievably cheap.

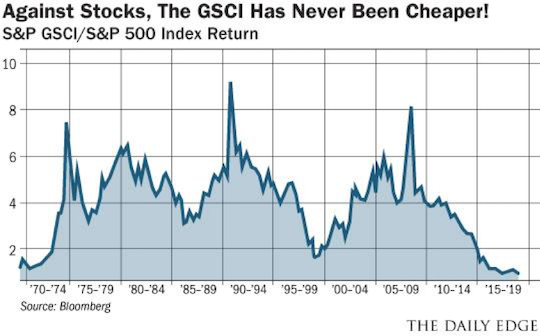

To support that fact, we demonstrated how the Goldman Sachs Commodity Index (GSCI), which tracks a basket of different commodity prices, was trading at a historically low valuation relative to the S&P 500.

The chart alone made a pretty compelling case for buying commodities.

But in addition, there were also two supporting facts that we thought really made buying commodities a no-brainer:

Fact #1 — The last two times (early 1970s and late 1990s) that the GSCI was priced this low relative to the S&P 500, it outperformed the S&P by nearly TENFOLD in the following few years.

Fact #2 — Equally important, over the half century covered by the data, the GSCI had never gone down relative to the S&P 500 from where it was in January of this year.

Put these two points together and you have investment nirvana.

— RECOMMENDED —

Experienced Biotech stock investor, Kyle Dennis, will be showing you 3 easy-to-follow steps that you’re going to want in your playbook & he’s got the numbers to prove it!

History was telling us that the upside potential from this valuation was huge — the GSCI outperforming the S&P 500 by a factor of 10.

Meanwhile, history was also showing that the downside from this valuation was non-existent!

Massive upside and no downside.

As I said — investment nirvana.

Not Just One Chart With A Screaming Buy Signal — But Two!

The GSCI being valued at historic lows relative to the S&P told us where to look for value.

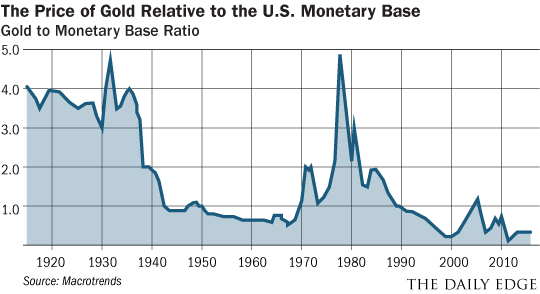

When we zeroed in on the sector for a closer look in January, what we found was a second chart that told us specifically what commodity we should be buying.

Just as the first chart told us that commodities were historically cheap relative to the S&P 500, this second chart told us that gold was historically inexpensive relative to the size of the American monetary base.

The conclusion that we reached was not difficult to get to.

Not only was there a lot of upside potential in commodities, there specifically was a lot of upside potential in gold — especially relative to the value of fiat currencies in this world of bloated central bank balance sheets.

The only question was which gold-focused investment was the best way to play this trade?

— RECOMMENDED —

Get Out of Cash Now

Former hedge fund manager with a long track record of accurate predictions says a huge shift is coming towards the U.S. stock market in as little as 6 months that will determine who gets wealthy in America and who gets left behind.

Sandstorm Gold is Our Best Way to Play This Trade

With the entire commodity sector a screaming buy (gold especially), we identified the royalty streaming company Sandstorm Gold (SAND) as the best way to play this opportunity.

So far so good with that trade.

Sandstorm shares are up roughly 20% since January.

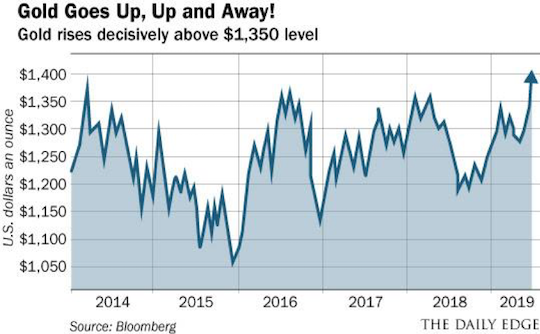

But with gold now breaking out sharply from its multi-year trading range below $1,350 per ounce, we still think Sandstorm Gold has significant upside.

What we find especially appealing about Sandstorm is its royalty streaming business model.

A royalty streaming company doesn’t produce gold itself.

Instead, these companies own “royalties” on the revenue generated from gold mining companies — the more they produce, the more royalty streaming companies get paid!

These royalty rights are received in exchange for providing development capital to the companies that mine the gold.

The most attractive attribute about a royalty business is what it doesn’t have. That would include long term debt, capital spending requirements or many employees.

These are capital light, low overhead, cash flowing businesses. The royalty business model involves almost no cash going out the door.

The royalty rights owned by these companies essentially entitle them to a tax payment (a royalty) on any revenue generated from gold production by the underlying gold miner.

I imagine a day in the office of a royalty streaming business consisting of opening the mail and depositing the royalty check in the bank.

In other words, the ultimate dream job!

Over the next three years, the gold production that Sandstorm has a royalty interest in is expected to more than double, which will do the same thing for Sandstorm’s cash flow.

And with gold prices soaring, those may turn out to be very conservative estimates.

That upcoming big increase in cash flow is not even close to being priced into Sandstorm’s current share price.

While publicly traded royalty streaming peers trade at 12 to 19 times EBITDA (earnings before interest, taxes, depreciation and amortization), Sandstorm trades at just 6 times the cash flow expected after this production jump.

To be valued in line with the average of its peer group, Sandstorm will still need to see its share price TRIPLE by 2022.